If a company is currently “hitting the wall”, even though it has made good progress in optimising its productivity, then it has probably overlooked one particularly important component: the right way to deal with uncertainty when planning its path to the goal.

- Part 1: Effectiveness vs. organisational structure

- Part 2: Efficiency vs. agility

- Part 3: Productivity/economic profitability vs. period thinking

- Part 4: Strategic uncertainty vs. economic profitability

In the last article, we took a critical look at the question of whether we can assess productivity based on periodic data. In the last part of the series of articles, we now address the question: what if our economic considerations are overshadowed by uncertainty?

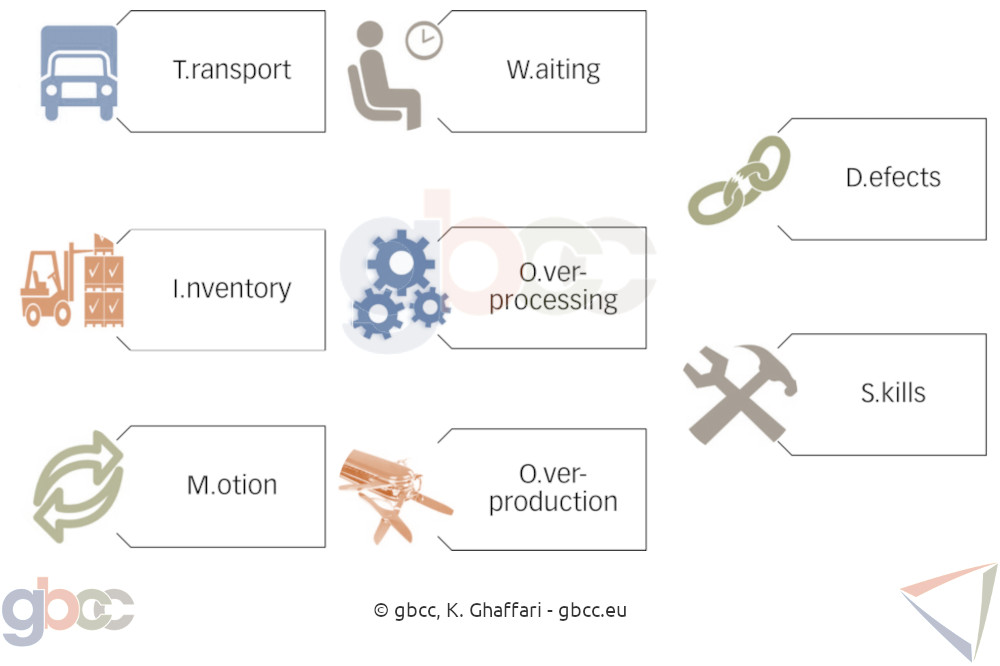

T.I.M. W.O.O.D.S.

Tim Woods is a memory hook in “Lean Management” to remember the eight forms of waste.

Let’s pick out two of them:

T stands for “transport”

The transport of workers or objects (raw materials, workpieces, finished products, tools, or operating resources) is possibly a necessary – but not value-adding – activity. Therefore, it is to be avoided.

And yet it has “always” been courteous for a company to relocate its own production to emerging countries and/or to purchase goods from the manufacturers there. The reason for this is obvious: the costs of production in emerging countries are so much lower than those say, in Germany, that this solution appears more economical for companies despite additional transport costs and time.

- However, one of the consequences of the coronavirus pandemic is that these companies are now facing serious supply chain disruptions.

I stands for “inventory”

What quantity of raw materials, goods being processed or finished products can one afford to keep in stock? In order to not tie up capital unnecessarily and unproductively, companies strive, for example, to bring in materials only when they are needed (just-in-time production). Currently, however, we are witnessing a shortage of materials in the construction industry that threatens the very existence of the companies. Prices have exploded, but materials are still not available.

- High inventories lying around unproductively would currently be a “waste” that the industry would dearly love to see.

How do these two realities come together? What takes precedence, risk awareness or productivity? Since 2021, the answer for German companies has been without a doubt risk awareness!

Risk management obligations of corporate management

The Corporate Stabilisation and Restructuring Act (StaRUG) came into force in Germany on 1st January 2021. It states:

“The members of the management body of a legal entity shall continuously monitor developments that may jeopardise the continued existence of the legal entity. If they recognise such developments, they shall take appropriate countermeasures. […]”

§ 1 (1) StaRUG

This is an appeal to look at the medium to long-term future of the company.

The appeal to think strategically about the right way to deal with uncertainty for both opportunities and risks.

The appeal to no longer be content with optimising the costs and revenues of the next reporting period.

To meet this requirement, companies need an early risk detection system to manage risks. However, this is what most medium-sized companies of today do not have, let alone use.

Risk in quality management

This requirement is by no means new, it is an integral part of quality management. Extract from ISO 9001:2015:

“[…] To conform to the requirements of this International Standard, an organisation needs to plan and implement actions to address risks and opportunities. Addressing both risks and opportunities establishes a basis for increasing the effectiveness of the quality management system, achieving improved results and preventing negative effects. […]”

That being said, in the example above, could the construction industry have anticipated this development? Could it have taken timely countermeasures? For example, by stocking up their own warehouses at an early stage? Of course! Especially since risk management experts have been trying to raise awareness of precisely such risks for many years. It has been in vain though; they have not been listened to in the past.

From SMEs to large corporations, companies tend to deal with the consequences of their business decisions only when they occur, not before.

Strategic decisions under uncertainty

Step 1: Planning the future

It all starts with setting up a realistic plan for the next three (or more) years. This is based on a realistic order intake and considers the available resources for financing and order processing.

Step 2: Identifying risks, making them measurable and aggregating them

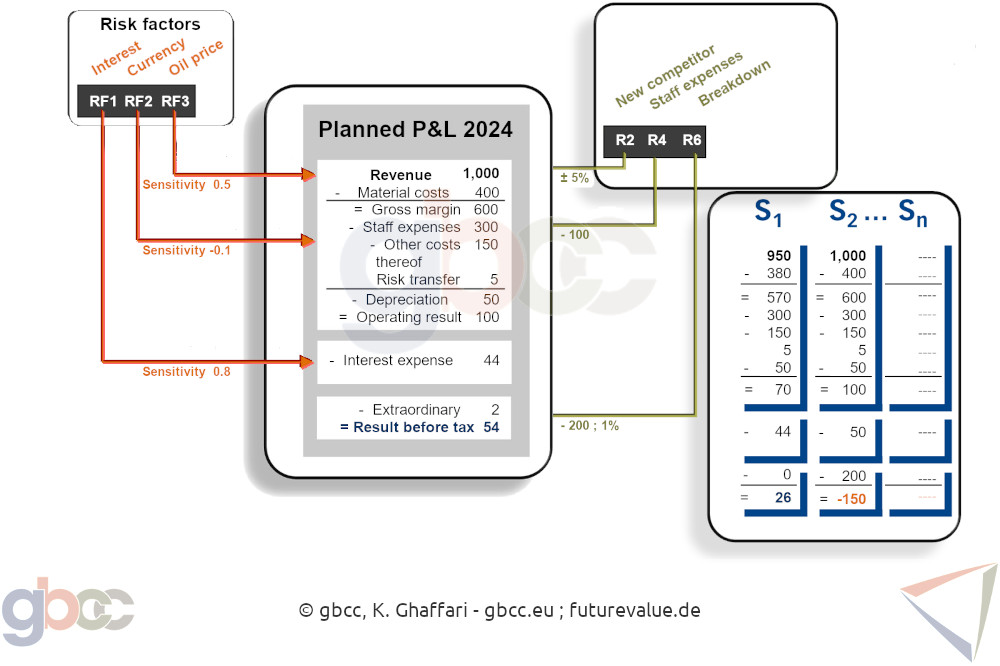

The next step is for all key people in the company to work together to systematically identify all significant risk factors. These are all factors that could cause one to deviate from one’s target figures, whether positive or negative. These include:

- The usual range of fluctuation of the individual items in the budgeted accounts.

- The occurrence of an event, such as a supplier failure.

- External risk factors and their influence on the individual positions, such as currency or interest rate developments.

Now, it is time to calculate scenarios as we can manage what we can measure! Even with a medium-sized company, it is advisable to use a simulation technique for this purpose. Equipped with assumptions, the software calculates thousands of scenarios and shows the balance sheet and P&L for the planning period on a probability distribution.

Step 3: Defining countermeasures

Let’s address a common misunderstanding. Management is not legally required to eliminate risks – be it by foregoing opportunities or by hedging the associated risks at a cost. The call is to deal analytically with the uncertainty of the business, so that we can consciously decide which opportunities and risks we can afford. The information and insights from the simulation make this decision much easier.

In this context, another misunderstanding should also be mentioned: every strategic decision that we make under uncertainty is nothing but a bet that we place. The management team will not have to deal with any backlash if the bet does not work out, but they might be reprimanded if they cannot demonstrate that they have consciously analysed their opportunities and risks before placing the bet. In the case of strategic decisions, it is therefore advisable to document the decision-making process in a way that is comprehensible to third parties.

Step 4: Verifying the effectiveness of the work

Our strategic decisions that take uncertainty into account have, of course, a huge impact on our future operational goals that we want to strive for. Let’s assume that we decide to massively increase our equity capital to be able to withstand higher future fluctuations in business without being dependent on external financing. We may have identified the behaviour of our house bank also as a risk factor. Indeed, some banks tend to hand out an umbrella when it’s sunny and then want to take it away when it rains.

The goal of increasing the equity ratio is thus outside the scope and is not the subject of an economic-profitability analysis. It is therefore completely irrelevant if a consultant calculates for us that we could increase the enterprise value by replacing equity capital with debt capital. We now know better!

Or let’s assume that we make the strategic decision to keep a high quantity of a product in stock. Then it is just as irrelevant if inventory-optimisation software computes that we could manage with much less quantity. Again, we know better!

However, our strategic decisions have consequences that must be considered to determine the appropriate path to the goal. Will it be necessary to enforce higher prices in the future? And/or to break off more consistently from ineffective processes and unsuitable customers? This is where the previously discussed considerations regarding effectiveness come in. These should be drawn up and reviewed together with the employees.

Step 5: Optimising the efficiency of the work

Only when effectiveness has been positively clarified does the question of increasing efficiency arise. This also includes possible digitalisation and automation campaigns. Such measures only make sense/add value when the previously mentioned steps have been worked through.

This brings us to the end of the series of articles. I hope that I have succeeded a little in making the complex interrelationships more accessible to you. However, one important component is still missing: the human factor! After all, companies are made up of people with all their egoisms, peculiarities, and quirks. The influence of the human factor is a complex topic in itself, which would have gone beyond the scope of this series of articles. But perhaps it is the right topic to tailor for your company over the course of an in-house workshop?

Thank you for your attention and feel free to get in contact regarding any questions, whether it’s about the article or about my services.